GHG Accounting

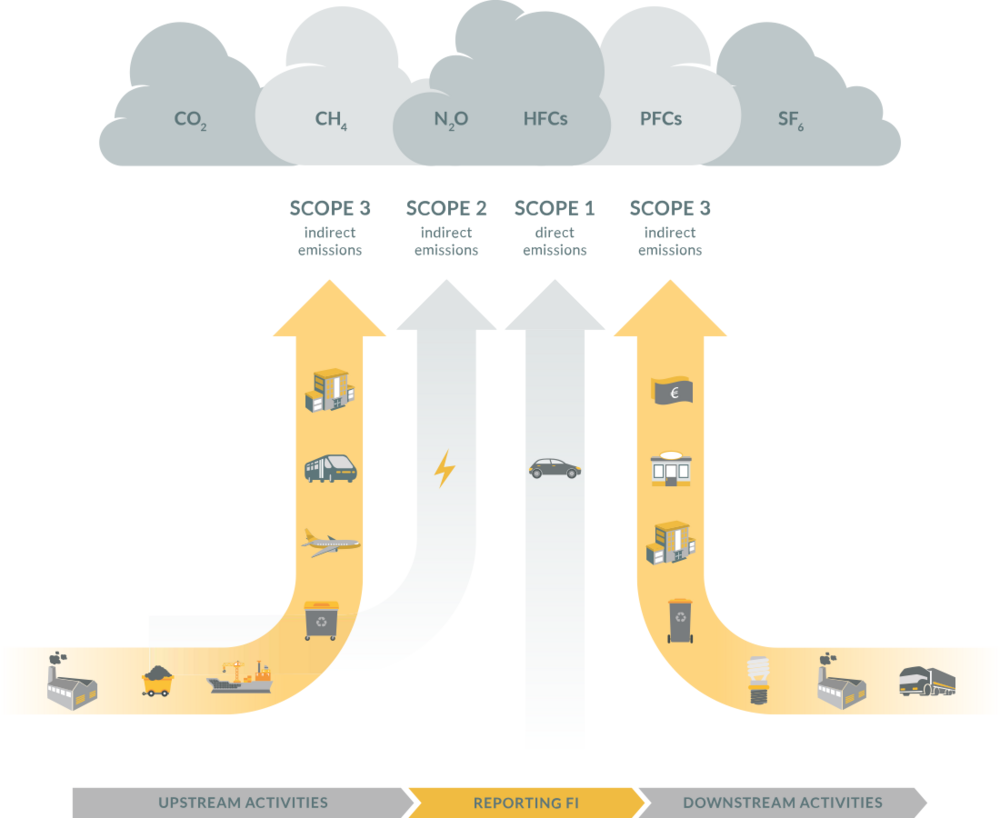

Many financial institutions and portfolio managers are lacking both a methodological approach and an adequate software tool to calculate their entire carbon footprint. In their sustainability reports, if at all only the so-called Scope 1 and Scope 2 emissions, i.e., emissions that arise from the energy consumption of the business, are presented. For financial institutions however, these emissions represent only a fraction of their total carbon footprint.

Instead, the Scope 3 emissions associated with the financing by the institutions are much more relevant. For this reason, a meaningful assessment of the total emissions of a financial institution can only be made by including Scope 3.

According to the GHG Protocol (category 15 investments), two complementary approaches are pursued: on the one hand, a top-down approach which applies sector-specific emission intensities and, on the other hand, a bottom-up approach, which determines the investment or loan-specific carbon footprint based on a set of limited and easily accessible project data. Bottom-up calculations generally reflect the financing purpose more precisely and should therefore be applied to sectoral priority areas of credit and investment portfolios. They are already available for important physical assets such as buildings, vehicles, aircrafts, ships and renewable energy. In order to obtain a comprehensive evaluation of overall Scope 3 emissions, the top-down approach is applied to calculate the remaining areas of the portfolios. The top-down approach can also be applied for financings with unknown purposes and/or insufficient data availability.

As a result, the carbon footprint of a portfolio can be presented by individual financings, by economic sector or by other specifications. The consideration of other greenhouse gases, such as methane (CH4) or nitrous oxide (N2O) is also possible. Since the Scope 3 emissions of financial institutions correspond to the Scope 1 and Scope 2 emissions of the financed assets and undertakings of their clients, there are two main areas of application: On the one hand, the quantification supports the financial institutions in the process of defining, target setting, monitoring and reporting their GHG emissions. Besides this, the tool also supports the identification of various benchmarks. On the other hand, financial institutions can also promote climate-compliant business development by actively approaching their clients and offering a quick assessment of their GHG footprint and the climate impact of the planned investments.